How Are BTR Rents and Incentives Shifting Under Renters' Reform?

As operators respond to the Renters’ Rights Bill, we have tracked advertised BTR rents in recent months to assess pricing behaviour alongside rising incentives, revealing a mixed performance across key markets.

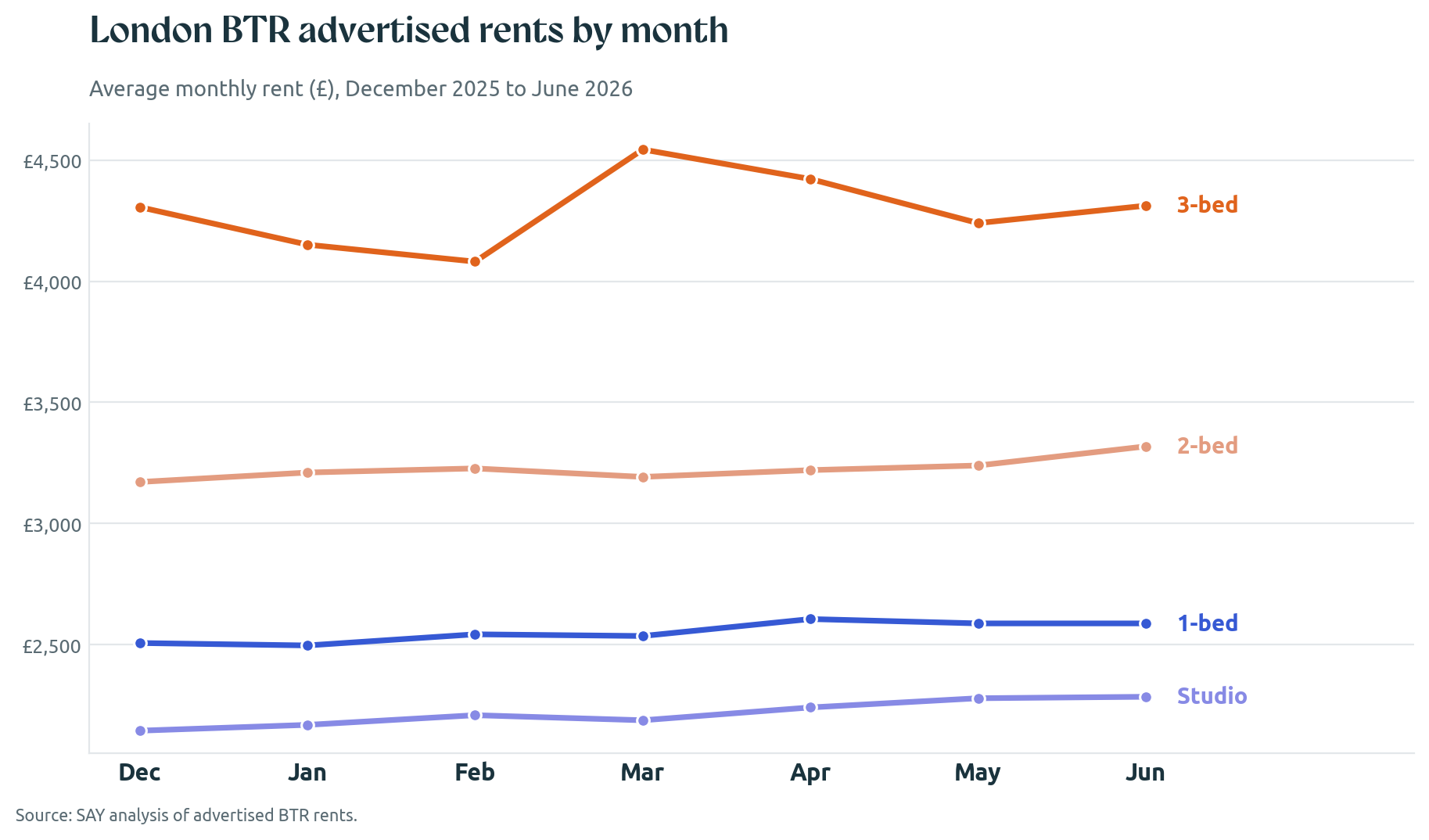

London

BTR rents in London continued to rise over the past six months, despite some short-term volatility across individual unit types. Studio rents increased from an average of £2,144 in December to £2,278 in May (+6.3%, +£134), while 1-bed rents followed a similar trajectory, rising by c.3.2% (+£81) to £2,587.

Growth in 2-bed rents was more modest (+2.2%), suggesting some degree of pricing resistance at higher price points. By contrast, the 3-bed market experienced greater volatility, declining through January and February before peaking in March and easing back to £4,240 in May. Despite these fluctuations, 3-bed rents remained broadly in line with the start of the year (-1.5% overall), indicating that demand for larger homes may be less consistent and more sensitive to affordability pressures than demand for smaller units.

Overall, the data points to resilient rental growth across London's BTR sector, particularly among smaller unit types. The divergence in performance suggests operators have been most successful in driving rental growth for studios and 1-bed homes, while larger units are encountering a more price-sensitive market. Nevertheless, rents across all unit types have remained broadly stable or increased, indicating continued pricing confidence among operators despite ongoing uncertainty surrounding rental market reforms.

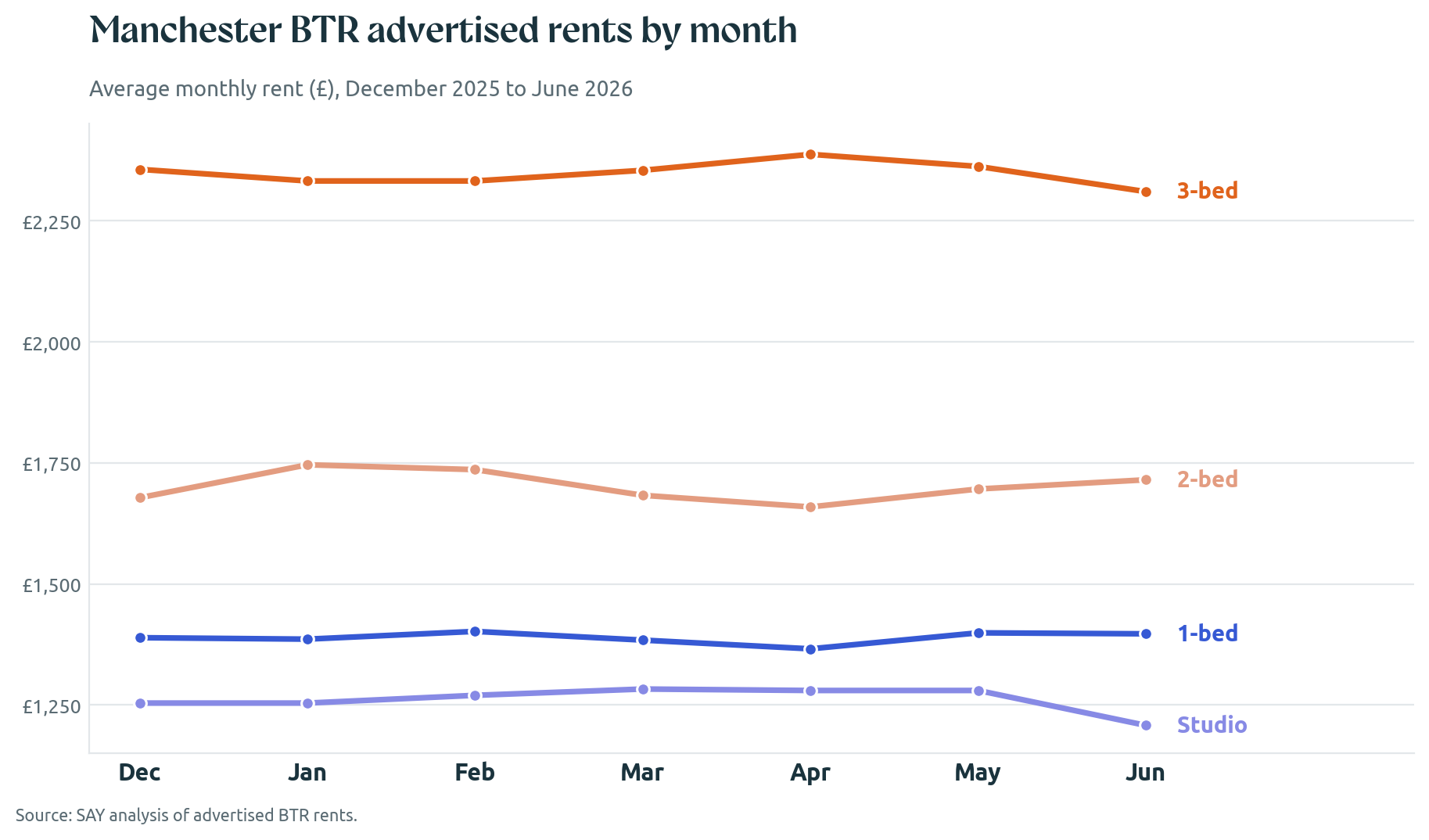

Manchester

Manchester presents a more stable picture than London, with only modest rental growth recorded across all unit types over the past six months. 1-bed rents remained broadly unchanged, increasing from an average of £1,389 in December to £1,399 in May (+0.7%, +£10), while 2-bed rents followed a similar pattern, rising by 1.1% (+£18) over the same period.

The 3-bed segment also demonstrated a high degree of stability, with average rents increasing marginally from £2,356 in December to £2,362 in May (+0.3%, +£6). Unlike London, where larger units experienced greater volatility, Manchester's family-sized homes remained largely insulated from short-term fluctuations, suggesting a more balanced relationship between supply and demand across the size spectrum.

Overall, the data points to a market characterised by pricing stability rather than significant rental growth. While there is evidence of modest upward pressure across the most active segments of the market, rental performance has remained relatively consistent regardless of unit size. This contrasts with the more pronounced divergence observed in London and suggests that operators in Manchester have adopted a measured approach to pricing. Despite ongoing uncertainty surrounding rental market reforms, rents have remained resilient, indicating continued confidence in underlying demand, albeit with more limited scope for rental growth than in the capital.

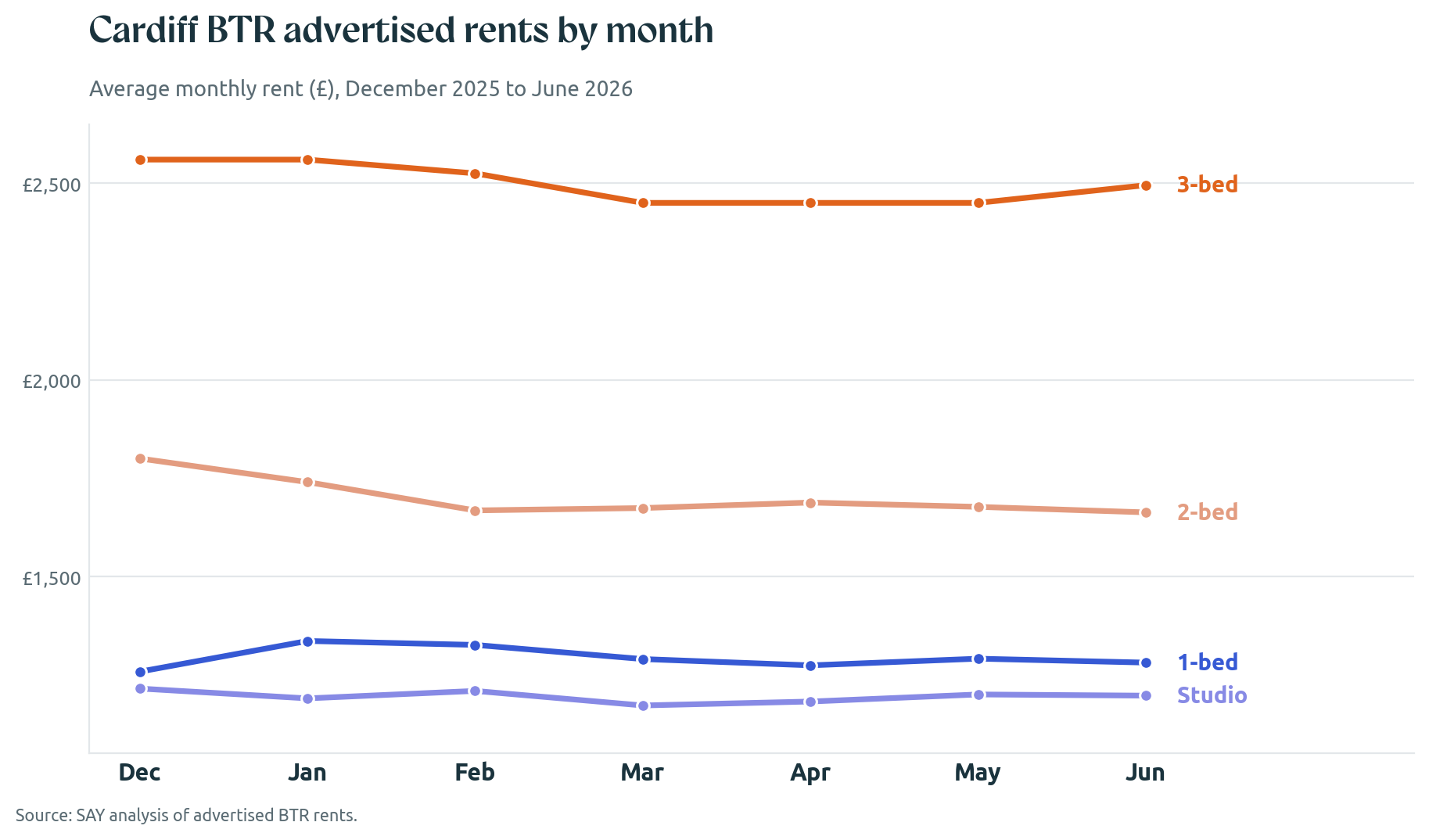

Cardiff

Cardiff has shown a softer rental performance than both London and Manchester, with rents generally easing since the start of the year. The 1-bed market experienced a strong uplift in January before gradually moderating, settling at £1,291 in May. While this still represents growth of 2.6% compared with December levels, the trend over recent months points to weakening pricing momentum following an early-year peak.

The adjustment has been more pronounced in the 2-bed segment, where average rents have fallen from £1,800 in December to £1,677 in May (-6.9%, -£123). This sustained decline suggests that demand at higher price points has softened. In the lead-up to the Renters’ Rights Bill, the figures suggest that maintaining occupancy may have become a greater priority than driving rental growth.

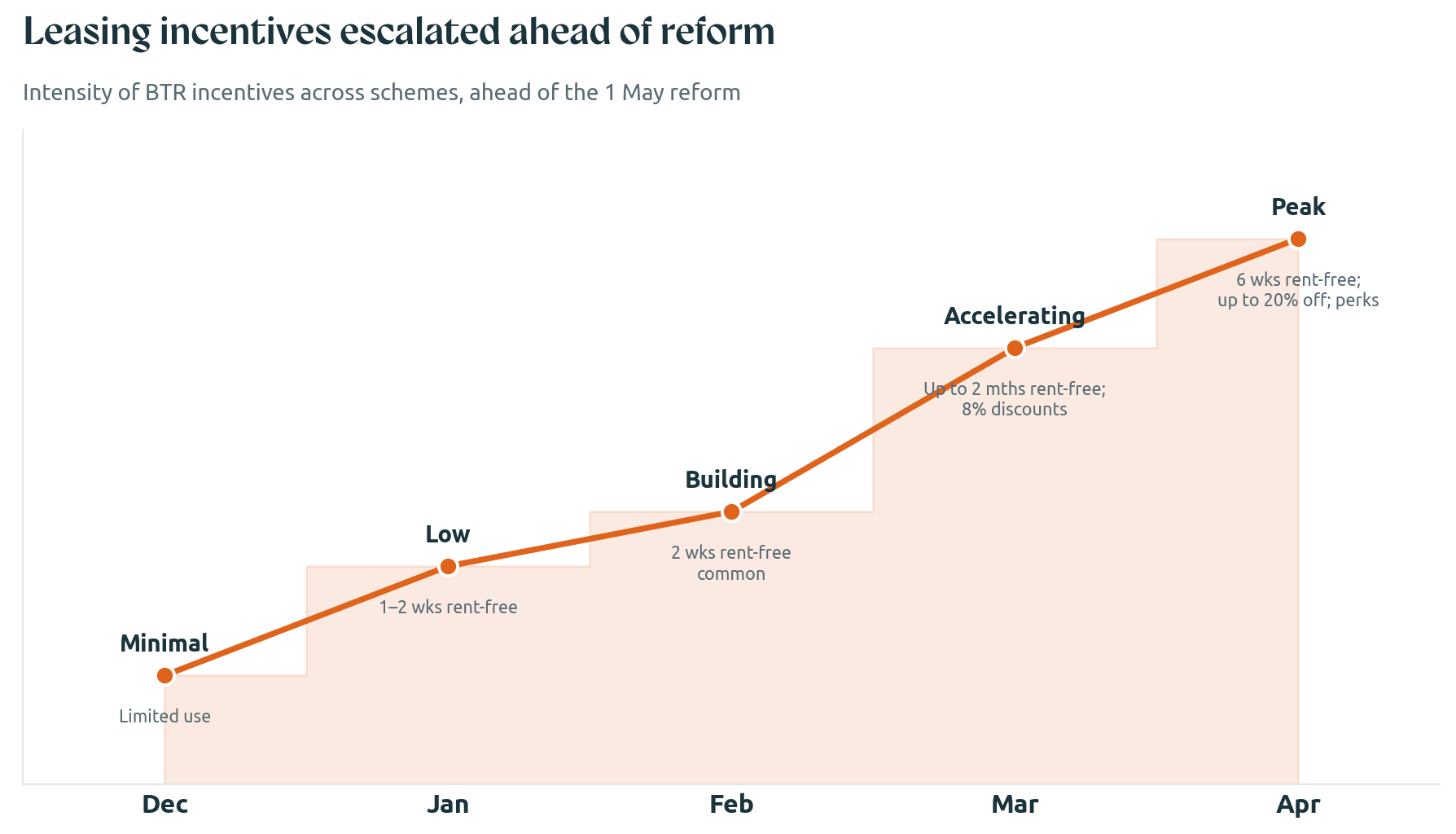

The use of Incentives

In the lead-up to the anticipated implementation of the Renters’ Rights Bill on 1st May, Build-to-Rent operators across all key markets notably increased their use of leasing incentives. This reflects a clear strategy to secure tenancies under existing terms before the legislative changes took effect. Based on schemes we have assessed, the progression of incentives has been both deliberate and increasingly aggressive:

December

Limited use of incentives

January

Initial uptick in incentives, aligned with seasonally slower leasing activity in January. Incentives used here are consistent with normal market conditions rather than policy-driven behaviour.

Predominantly short rent-free periods (typically 1–2 weeks)

February

Increased adoption of incentives across schemes

Two weeks’ rent-free becoming more common

Early signs of operators responding to upcoming regulatory change

March

Significant acceleration in both the scale and variety of incentives

Examples include: 4 weeks’ rent-free for move-ins before a specified date, 8% discount on rent tied to pre-deadline move-ins, Up to 2 months’ rent-free, continued use of shorter-term incentives.

Clear evidence of operators competing more aggressively to secure tenants

April

Peak incentive activity observed across the schemes analysed

Wide-ranging and highly competitive offers, including:

1 month’s rent-free for move-ins before May

Extended or enhanced versions of March incentives

8%–16% discounts on monthly rent

20% rental discounts in some cases

Structured offers (e.g. 50% off month 1 and 50% off month 12)

6 weeks’ rent-free

Value-add incentives such as free gym membership

Additional perks (e.g. £150 vouchers alongside rent-free periods)

Strong indication of urgency among operators to transact ahead of the legislative deadline

The data demonstrates a clear and accelerating trend, moving from minimal incentive use at the end of 2025 to highly competitive, multi-layered offers by April. This reflects a strategic push by BTR operators to de-risk leasing pipelines and secure occupancy ahead of the Renters’ Rights Bill reshaping the operating environment.

Notably, incentive-led leasing strategies have not disappeared following the introduction of the new regulations. Operators continue to deploy a range of offers across the market, suggesting that incentives remain an important tool for supporting lease-up, maintaining occupancy, and responding to local competitive pressures. As the sector adapts to the new regulatory framework, it will be important to monitor whether incentives remain a core component of leasing strategies or gradually reduce as operators gain confidence in the post-reform environment.

As the market continues to evolve in response to regulatory change, understanding how rents and incentives are shifting at both scheme and unit level is becoming increasingly important. Access to detailed, real-time data, alongside deeper insight into local rental performance and tenant demographics, can help operators and investors make more informed decisions around pricing, positioning, and lease-up strategy.

Alongside this, the Renters’ Rights Bill is expected to place greater emphasis on transparency and evidence-based rent reviews. As landlords and operators navigate this changing landscape, robust evidence packs that clearly demonstrate how proposed rent increases align with local market conditions will become increasingly important. This is an area where we can provide support, combining granular market data with tailored analysis to help clients substantiate rental positioning with confidence.

If you would like to explore how these trends, or our wider market reporting and analysis, may impact your asset or pipeline, please get in touch with our team.

Frequently Asked Questions

How have BTR rents changed in the run up to the Renters' Rights reforms?

Performance has varied by market. In London, advertised rents trended upwards over six months, with studios up 6.3% and 1 beds up around 3.2%, though larger units showed more volatility. Manchester remained stable across all unit types, with growth of 1% or less. Cardiff softened, with 2 bed rents falling 6.9% between December and May. The picture points to resilient growth in smaller London units alongside greater price sensitivity elsewhere.

Why did operators increase the use of incentives?

In the lead up to the anticipated implementation of the reforms, operators across all key markets increased incentives to secure tenancies under existing terms before the changes took effect. This reflected a deliberate strategy to de-risk leasing pipelines and protect occupancy ahead of a shifting operating environment.

What kinds of incentives were most common?

Incentives escalated from short rent-free periods of one to two weeks in early 2026 to wide-ranging offers by April. These included up to two months rent-free, rental discounts of 8% to 20%, structured offers such as 50% off the first and final month, six weeks rent-free, and value-add perks like free gym membership and vouchers.

Are incentives likely to continue now the reforms are in place?

Incentive-led leasing has not disappeared following the introduction of the new regulations, and operators continue to deploy a range of offers. Whether incentives remain central to leasing strategy or gradually reduce will depend on how quickly operators build confidence in the post-reform environment. We will continue to monitor both their prevalence and structure over the coming months.

How will the reforms affect rent reviews?

The reforms are expected to place greater emphasis on transparency and evidence-based rent reviews. Landlords and operators will increasingly need robust evidence packs that demonstrate how proposed increases align with local market conditions.

How can SAY Property help operators navigate these changes?

We combine granular, real-time market data with tailored analysis to help operators and investors make informed decisions on pricing, positioning, and lease-up strategy. We also support clients in building evidence packs that substantiate rental positioning with confidence.